Colliers are calling it an exciting year for commercial property, supported by a general election on the horizon and an economic gear shift towards a period of sustained growth. The following pages summarize their research and analysis

The Kiwi economy

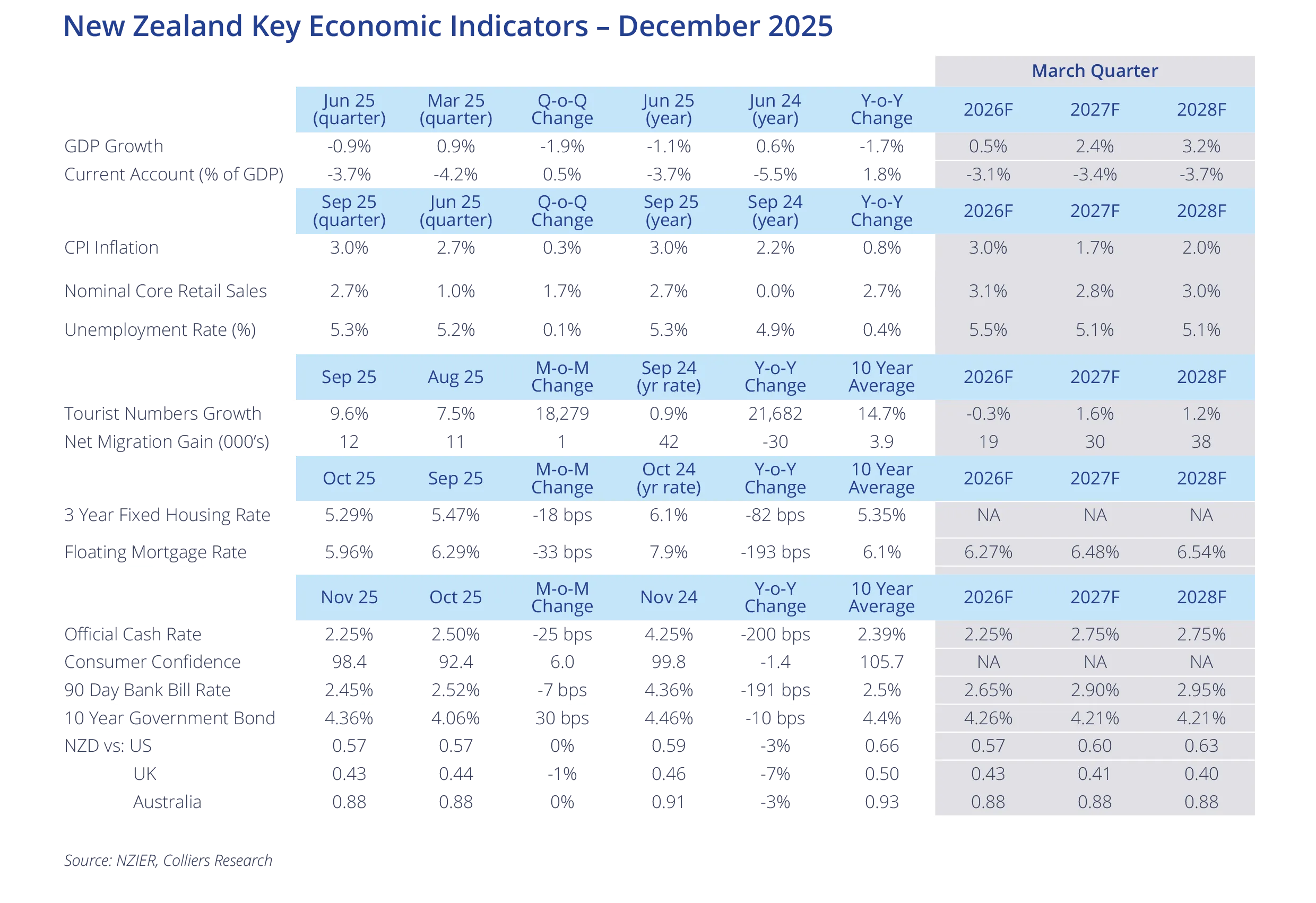

Interest rates have more than halved over the past year and are now supporting economic activity.

The weak economic performance of 2025 will be replaced by a sustained recovery over 2026, with economic growth averaging around 2.5 percent expected.

High-frequency indicators such as electronic card spending and traffic data are already rising. The strengthening economy, increased investment, and lower unemployment will drive increased momentum in property markets.

Economic risks are to the downside. New Zealand enters 2026 amid heightened geopolitical tensions, ongoing trade disputes between the USA and China and increased unease about the valuation of tech stocks.

There are always risks to a projection and most of these risks never materialise, which is why Colliers is seeing investor and business confidence about activity for the next 12 months increase despite the risks.

Increased tourist demand in key centres

The outlook for economic growth in New Zealand’s trading partners firmed over 2025, there is likely to be more tourist demand for New Zealand.

International visitor arrivals are projected to keep rising slowly over 2026 and this supports demand in our markets more heavily geared towards international tourists, such as Rotorua and Queenstown.

Wellington, which relies more heavily on government spending, is expected to continue with subdued demand due to ongoing fiscal constraint.

Improving economic performance will support a recovery in business travel and in turn, hotel demand. The opening of the New Zealand International Convention Centre will boost hotel demand in Auckland as close to 100 events are pre-booked for 2026.

The industrial sector

Demand for new prime grade industrial space will drive benchmark rentals

Leasing

Leasing activity will lift as economic growth gathers momentum and increased business investment drives up demand for industrial space. This will cause vacancy rates to ease further off their already strong base.

Upward pressure on rental rates for existing premises will begin to emerge. However, current vacancy levels, combined with the availability of sublease options will see this lagging the increase in leasing activity.

Industrial land will be absorbed as the owner occupier market regains confidence; demand for new prime grade space will drive new benchmark rentals reflecting the cost of development.

Investment Sales

Term deposit rates have decreased and are expected to remain at low levels over 2026, meaning savvy investors will be looking for alternative investments to ensure stable returns.

Commercial property yields offer these more attractive returns, and we anticipate that with $205 billion of deposits set to reprice at lower rates in the next 12 months we will see increased investment and sales activity across the commercial property market.

Office

Demand for prime office spaces will strengthen as businesses swing back to a preference for having staff in the office

Flexible working options has curtailed demand for office space in the post-pandemic years, but this is changing and we expect this shift to persist into 2026 as businesses swing back towards a preference for having staff in the office.

Demand for prime office spaces will strengthen off the back of this trend shift as employers try to sweeten the return-to-office mandates by offering enhanced amenities. The ‘flight to quality’ dynamic will persist through 2026.

As the economy enters a period of recovery and expansion, the creative destruction cycle will shift in favour of new business creation.

When businesses start out, they typically have smaller operations and will initially add to demand for secondary spaces. Colliers expects this dynamic will support demand for secondary office space and absorb some of the vacant space that has emerged during recent years.

The 2026 opening of New Zealand’s first underground rail system, Auckland’s City Rail Link, will shift demand patterns for office spaces in the Supercity.

With an end to construction-related disruptions and enhanced connectivity we expect to see increased demand and reduced vacancies around these new transport links.

This is just one example of how newly completed infrastructure projects will continue to shape changes in demand patterns across the country in the year ahead.

Retail

Large format retail is predicted to continue to outperform the rest of the market

Consumption spending is expected to grow at roughly 0.6 percent each quarter in 2026 as pressure on household incomes eases in a lower inflation and lower interest rate environment.

The trend to smaller but more frequent spending is expected to moderate as cost-of-living pressures continue to subside. North Island markets have underperformed over 2025 and therefore will experience stronger growth in 2026 as they recover.

Large format retail will continue to outperform the rest of the market as consumers continue to demand a wide range of products. International brands will continue to explore opportunities to expand in the New Zealand market.

Consumer preferences will continue drifting towards an increased focus on sustainability, and financial considerations will drive further store optimisation.

Online retailing continues to grow, but Colliers do not see this trend radically changing the way we shop in 2026. The real estate specialist anticipates increased competition for premises within prime retail precincts and upward pressure on rental rates.

Rural

The dairy sector has had a stellar 2025, but we expect this to moderate in 2026. Export prices for dairy products are drifting down from record highs, and we expect the farmgate milk price to land slightly below the $10/kgMS that Fonterra is guiding.

Despite this, we expect a strong year ahead as farmers have consolidated their debt over 2025 and the recent Fonterra payouts will provide a substantial influx of cash into the sector.

Our horticultural and meat exports are proving to be resilient to the US tariff induced trade volatility. We expect 2026 to carry over this strong demand and boost the revenue of our rural communities.

This in turn provides strong demand for commercial sales and leasing in the provinces.

Wood and wood product exports face a year of slow demand ahead as China’s economy continues to come to terms with a construction oversupply and a slowing development market.

Specialist markets

New Zealand’s not getting any younger. In 2026, there’s set to be 932,000 people aged 65 or older in New Zealand.

That’s an additional 30,000 people compared to 2025. This is a long-term trend that will continue to drive demand in the specialist health and care segment of commercial property.

At the other end of the age spectrum, there are record high numbers of student visa arrivals into New Zealand and a high youth unemployment rate is encouraging young people domestically to stay in education for longer.

This provides solid demand for purpose-built student accommodation and investment into our education sector and is expected to encourage new development in 2026.

To read more insights from Colliers click here.